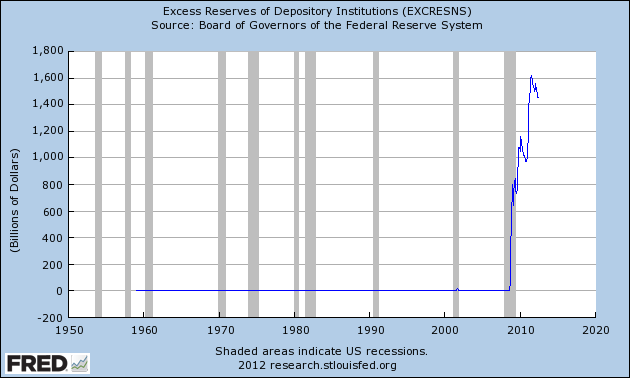

Its not hard to figure out where this base demand is coming from: member banks have increased holdings of excess reserves at the Fed dramatically. See below.

Maybe it has something to do with the fact that the Fed is paying them 0.25% on those reserves. Accounts at the Fed are where money goes todie sit, not get lent out to businesses or circulated by consumers. Ordinarily, banks keep some reserves at the Fed to meet their reserve requirement, not stash hundreds of billions there.

Why, then, would Bernanke's regime implement such a contractionary policy? Its because the Fed has, since 2008, been much more interested in setting what John Cochrane called "financial policy" than monetary policy. While indicators such as below-trend inflation, high unemployment, and low NGDP growth would scream for more monetary expansion, the Fed has been intent to manipulate specific portions of financial markets. For example, below is the Fed's holdings of mortgage backed securities.

Maybe it has something to do with the fact that the Fed is paying them 0.25% on those reserves. Accounts at the Fed are where money goes to

Why, then, would Bernanke's regime implement such a contractionary policy? Its because the Fed has, since 2008, been much more interested in setting what John Cochrane called "financial policy" than monetary policy. While indicators such as below-trend inflation, high unemployment, and low NGDP growth would scream for more monetary expansion, the Fed has been intent to manipulate specific portions of financial markets. For example, below is the Fed's holdings of mortgage backed securities.

No comments:

Post a Comment